Before a jumbo mortgage application, cut card balances below 10%, avoid new credit, and ask your lender about rapid rescoring to capture score gains fast.

Dispute unpaid medical debt in writing, deny admitting liability, and avoid partial payments or new promises until verifying whether the statute of limitations has expired.

After a high-net-worth divorce, rebuild prime credit by separating joint liabilities, verifying asset-transfer reporting, and reestablishing low-utilization accounts in your name.

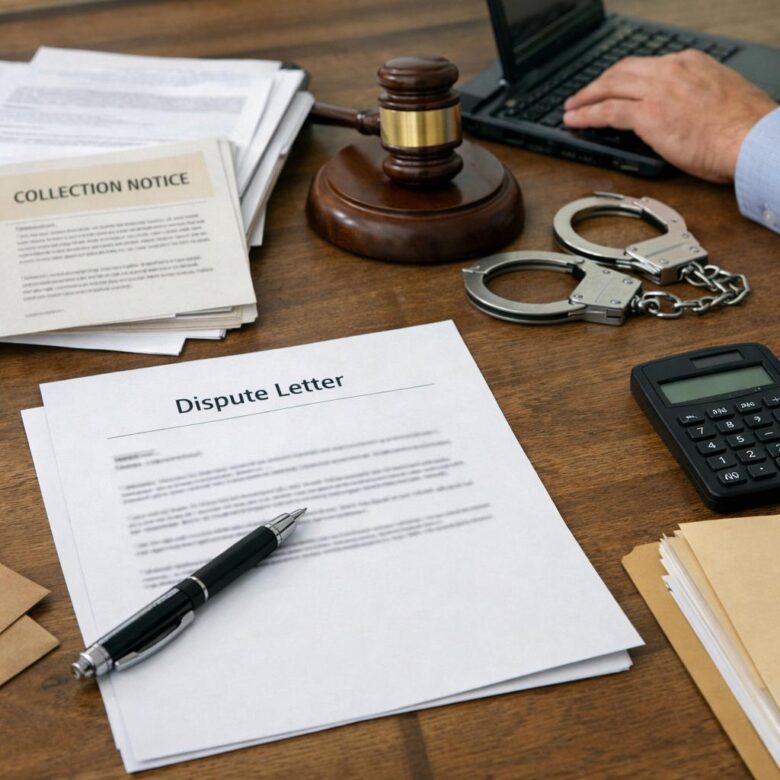

Use a written FCRA dispute to demand the bureau verify a stale collection’s date, ownership, and balance. If it cannot document accuracy, it must correct or delete the account.

Cut utilization fast: target cards nearest 30%, make mid-cycle payments before statement close, shift balances strategically, and request limit increases only where spending is controlled.